Family questions, heir concerns, and conversation guides.

“My parent is considering a reverse mortgage, and I want to make sure they understand what they are doing.”

That concern usually comes from a good place.

You may be worried that your parent could lose the home, misunderstand the costs, reduce an expected inheritance, or agree to something without seeing the full picture.

Those are reasonable questions.

But let’s slow the conversation down.

The best first step is not to immediately support or oppose the idea. It is to understand why your parent is exploring it, how the loan works, what responsibilities remain, and what alternatives should also be considered.

The goal is not for the family to pressure the parent into—or out of—a reverse mortgage.

The goal is clarity.

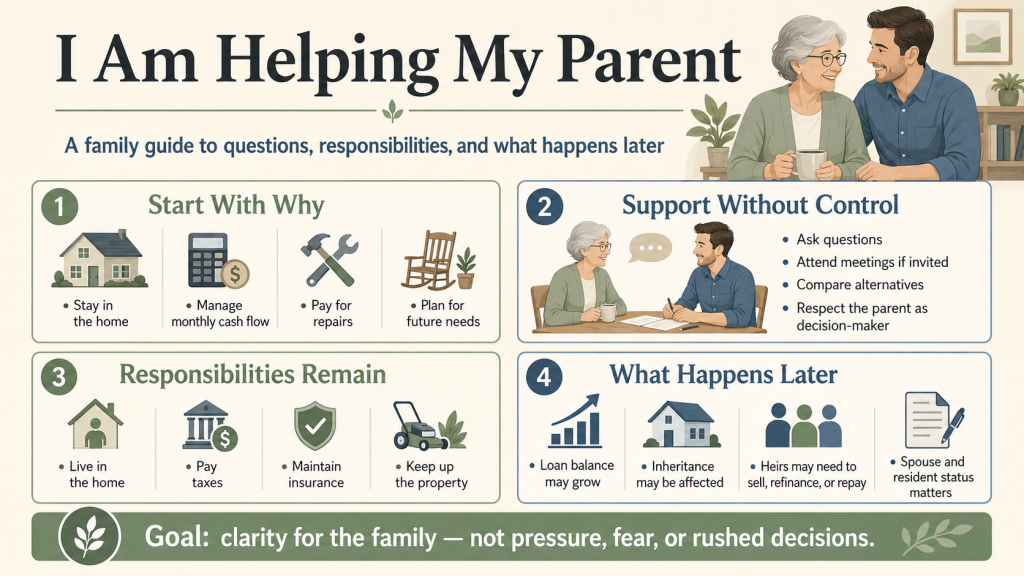

Begin With Why Your Parent Is Asking

A reverse mortgage is a financial product, but the reason someone considers one is usually personal.

Your parent may be thinking about:

- Remaining in the home

- Managing an existing mortgage payment

- Paying for necessary repairs

- Creating more room in the monthly budget

- Preparing for future home or care needs

- Avoiding the sale of other assets at an inconvenient time

- Helping a spouse remain in the home

- Establishing access to funds for unexpected expenses

- Buying a different home that better fits retirement needs

Before debating the loan, ask:

“What are you hoping this would help you accomplish?”

That question changes the entire conversation.

Once the real goal is clear, the family can compare a reverse mortgage with other possible options instead of treating the product itself as the goal.

Your Parent Is Still the Decision-Maker

Adult children often become involved because they want to protect a parent.

That is understandable, but the home belongs to the parent, and the financial decision is generally theirs to make as long as they have the legal capacity to do so.

A productive family conversation respects that independence.

Your role may be to:

- Help gather information

- Attend educational meetings if your parent wants you there

- Take notes

- Ask questions your parent may not think to ask

- Help compare alternatives

- Encourage independent legal, financial, or tax advice

- Make sure important family members understand what may happen later

Your role is not to take over the conversation or assume that preserving an inheritance should be more important than your parent’s current needs.

The right balance is support without control.

Does the Bank Own the Home?

Generally, no.

With a reverse mortgage, the homeowner typically retains title to the property, subject to the mortgage lien and the terms of the loan.

The lender does not simply take ownership of the home because the loan closes.

However, retaining title also means the homeowner continues to have important responsibilities.

Those responsibilities should be understood clearly before any decision is made.

What Responsibilities Does My Parent Keep?

A reverse mortgage does not remove the basic obligations of homeownership.

The borrower generally must:

- Continue living in the home as a primary residence

- Pay property taxes

- Maintain required homeowners insurance

- Maintain applicable flood insurance

- Pay homeowners association or similar property charges

- Keep the property reasonably maintained

- Follow the occupancy and other requirements in the loan documents

Failure to meet the loan obligations may cause the reverse mortgage to become due and payable.

This is one of the most important points for families to understand.

A reverse mortgage may change how principal and interest are paid, but it does not make the ongoing costs of the home disappear.

Are Monthly Mortgage Payments Required?

Reverse mortgages generally do not require scheduled monthly principal-and-interest payments while the loan remains in good standing.

That statement needs context.

Interest and other permitted charges are generally added to the loan balance over time. The homeowner must continue paying required property charges and meeting the other loan obligations.

Your parent may also choose to make voluntary payments, subject to the loan terms, although those payments are generally not required in the same way they are with a traditional forward mortgage.

The safer way to understand it is:

A reverse mortgage may remove the requirement for scheduled monthly principal-and-interest payments, but it does not remove taxes, insurance, maintenance, association charges, utilities, or other homeownership costs.

What Happens to the Loan Balance?

A traditional mortgage balance usually declines as the borrower makes scheduled principal-and-interest payments.

A reverse mortgage generally works differently.

When the borrower does not make voluntary payments, interest and permitted charges are added to the loan balance. As a result, the balance generally increases over time.

That increasing balance usually means less home equity may remain later.

This does not automatically make the loan a poor choice. Your parent may decide that using some home equity now supports an important housing or financial goal.

But the family should understand the tradeoff:

Using equity today may reduce the equity that remains for the homeowner or the estate later.

Can a Reverse Mortgage Affect Inheritance?

Yes.

A reverse mortgage can affect inheritance because the loan balance generally must be repaid when it becomes due and payable.

If the home is sold, the reverse mortgage is ordinarily repaid from the sale proceeds. Any remaining equity, after repayment of the loan and other applicable costs or liens, generally belongs to the homeowner or the estate.

Because the reverse mortgage balance may increase over time, the amount of equity left in the home may be lower than it would have been without the loan.

That does not necessarily mean there will be no inheritance.

It means no one should assume what the remaining equity will be years from now.

The future value of the home, the growing loan balance, property expenses, market conditions, the amount borrowed, and the length of time the loan remains outstanding can all affect the result.

What Happens When My Parent Moves or Passes Away?

A reverse mortgage generally becomes due and payable after a maturity event described in the loan documents.

Examples may include:

- The last borrower selling the home

- The last borrower permanently leaving the home as a primary residence

- The last borrower passing away

- Failure to meet required loan obligations

When that occurs, the borrower, estate, or heirs generally need to work with the loan servicer.

Depending on the circumstances and loan terms, available options may include:

- Selling the home and repaying the reverse mortgage from the proceeds

- Repaying the loan from other available resources

- Refinancing the balance into another loan to retain the home

- Pursuing another option permitted by the loan documents or program

Requirements, valuations, notices, and deadlines can vary. The family should contact the servicer promptly after a maturity event and should not rely on general online information as a substitute for the actual loan documents.

Can the Children Keep the Home?

Possibly.

A reverse mortgage does not automatically prevent heirs from keeping the property.

However, keeping the home generally requires the reverse mortgage balance to be addressed. Heirs may need to repay or refinance the amount required under the loan and program terms.

Whether that is practical depends on:

- The loan balance

- The home’s value

- The heirs’ available funds

- The heirs’ ability to qualify for financing

- The property’s condition

- The number and interests of the heirs

- Estate documents

- Applicable loan requirements and timelines

If keeping the home is important to the family, discuss that goal before the reverse mortgage closes.

Ask what resources would realistically be available to repay or refinance the loan later.

Wanting to keep the house and being financially prepared to keep it are two different things.

Will the Children Personally Owe the Debt?

Do not assume the answer based on a general description of reverse mortgages.

Ask the mortgage professional to identify the exact product being considered and explain whether it is a non-recourse loan, what protections apply, and what the borrower or heirs could be required to repay under the actual loan documents.

HECM and proprietary reverse mortgage products may not have identical terms.

The family should review the proposed loan documents and consult an attorney when estate liability, title, trusts, or inheritance planning is a concern.

What About a Spouse or Other Person Living in the Home?

This deserves careful attention.

The rights of a spouse or other resident may depend on whether that person is:

- A borrower

- A co-owner

- An eligible or ineligible non-borrowing spouse

- Listed on the deed

- Named in a trust

- Merely residing in the property

- Protected under specific loan or program provisions

Living in the home does not, by itself, guarantee the right to remain there after the borrower moves or passes away.

Ask specifically:

- Who will be a borrower?

- Who currently holds title?

- Is there a non-borrowing spouse?

- What protections apply to that spouse?

- What conditions must be met for those protections to continue?

- What happens to another family member who lives in the home but is not a borrower?

This is an area where mortgage, estate-planning, and legal advice may need to work together.

Questions Adult Children Should Ask

A useful family discussion should cover more than “How much can my parent receive?”

Ask:

About the goal

- What problem is the reverse mortgage intended to solve?

- Is the need temporary or long-term?

- How long does my parent expect to remain in the home?

- Is the home physically and financially suitable for aging in place?

About the loan

- What type of reverse mortgage is being considered?

- How is eligibility determined?

- What costs would apply?

- How will the interest rate work?

- How will the balance change over time?

- How would any existing mortgage or liens be handled?

- How could the proceeds be received?

- Is counseling required?

About ongoing responsibilities

- Who will pay the property taxes and insurance?

- Can my parent realistically afford those expenses?

- Are major repairs likely?

- Is a set-aside or other arrangement required?

- What could cause the loan to become due and payable?

About the family

- Who is on title?

- Who will be a borrower?

- Is there a spouse who will not be a borrower?

- Does anyone else live in the home?

- Does the family hope to keep the property?

- How could the loan affect the estate?

- Who will communicate with the servicer later?

About alternatives

- Should the existing mortgage simply be kept?

- Would a traditional refinance be appropriate?

- Could a home-equity loan or line of credit work?

- Could expenses be reduced another way?

- Would selling or downsizing better support the long-term goal?

- What happens if the family makes no change?

A Family Meeting Guide

A good family meeting does not need to feel like an intervention.

Try this structure.

Step 1: Let the parent explain the goal

Begin with:

“Tell us what you are trying to accomplish.”

Let your parent speak before anyone offers an opinion.

Step 2: Separate facts from fears

Write down every concern.

Examples:

- “I am worried the bank will own the home.”

- “I am worried Mom will run out of equity.”

- “I am worried no one is planning for taxes or repairs.”

- “I am worried we will not know what to do later.”

Then identify which concerns are factual questions that can be answered and which are emotional concerns that need a larger family discussion.

Step 3: Review the homeowner’s responsibilities

Make sure everyone understands:

- Primary-residence requirements

- Property taxes

- Insurance

- Property maintenance

- Association charges

- How the loan balance changes

- Events that may cause the loan to become due

Step 4: Compare alternatives

Do not evaluate the reverse mortgage in a vacuum.

Compare the costs, benefits, limitations, and likely consequences of other available paths.

Step 5: Discuss what happens later

Talk openly about:

- Moving

- Long-term care

- The death of a borrower

- The surviving spouse

- The estate

- Whether anyone hopes to keep the home

- Who will handle notices and paperwork

Step 6: Write down unanswered questions

Bring those questions to the mortgage professional, housing counselor where applicable, and any legal, tax, financial, or estate-planning professionals involved.

No one needs to decide during the first meeting.

Helpful Documents to Gather

A family may benefit from gathering:

- A recent mortgage statement

- Statements for any home-equity loans or other property liens

- Property-tax information

- Homeowners and flood-insurance information

- Homeowners association information

- The deed or current title information

- Trust or estate documents, when relevant

- A list of people currently living in the home

- A basic household budget

- Information about expected repairs or accessibility changes

- Existing powers of attorney or legal-authority documents, when applicable

Do not send private documents through an unapproved website, email account, or messaging system.

Ask how sensitive information should be transmitted securely.

When Should Other Professionals Be Involved?

A reverse mortgage professional can explain the mortgage product, process, and loan requirements.

That person does not replace:

- An elder-law or estate-planning attorney

- A tax professional

- A financial advisor

- An insurance professional

- A benefits specialist

- An independent housing counselor

Other professionals may be especially important when the situation involves:

- A trust

- Multiple heirs

- A non-borrowing spouse

- Questions about mental capacity

- Medicaid or other public-benefit planning

- Tax consequences

- An existing life estate

- A family member living in the home

- A plan to preserve the property for future generations

- A power of attorney

- A guardianship or conservatorship

- Disagreement among family members

The mortgage is one part of the plan. It may not be the only part that matters.

Warning Signs That the Conversation Should Pause

Slow down if:

- Your parent cannot explain the basic loan obligations

- Someone is promising guaranteed approval or a guaranteed amount

- The presentation suggests the loan is free money

- Taxes, insurance, maintenance, or repayment are being brushed aside

- Someone is creating urgency or fear

- The family is told that heirs do not need to understand what happens later

- A spouse or resident’s status is unclear

- Costs are not being explained

- Alternatives are dismissed without discussion

- Your parent feels embarrassed, rushed, or pressured

- Someone asks for sensitive personal information through an unapproved channel

- The product is being presented as right for everyone

A sound decision can survive questions.

What Russ Would Want the Family to Understand

A reverse mortgage is not automatically a good decision or a bad decision.

It is a loan with costs, responsibilities, possible benefits, and long-term consequences.

For one family, it may help support an important goal.

For another, keeping the current mortgage, using another resource, selling, downsizing, or waiting may make more sense.

The family’s job is not to begin with a conclusion.

Begin with the parent’s goal. Understand the facts. Compare the options. Discuss what happens later.

Then make the decision with clear eyes.

Frequently Asked Questions

Should I attend the reverse mortgage meeting with my parent?

You may attend if your parent wants you involved and the mortgage professional permits it. Having a trusted family member present can help with note-taking and questions, but the homeowner should remain part of the conversation and understand the decision personally.

Does the bank own my parent’s home?

Generally, no. The homeowner typically retains title, subject to the mortgage lien and loan terms.

Can my parent lose the home?

A reverse mortgage includes continuing obligations. If the borrower fails to meet occupancy, tax, insurance, maintenance, or other loan requirements, the loan may become due and payable.

Will there be anything left for the heirs?

There may be, but no specific amount can be promised. The remaining equity will depend on the home’s future value, the loan balance, other liens, selling costs, and the length of time the loan remains outstanding.

Can I stop my parent from getting a reverse mortgage?

A legally capable homeowner generally makes their own financial decisions. Family members can ask questions, provide information, and encourage independent advice. Concerns about capacity, coercion, or abuse should be addressed with qualified legal or protective professionals.

Does my parent have to involve the children?

Not necessarily. However, family involvement can be helpful when the homeowner wants support or when the decision may affect a spouse, resident, estate plan, or expectation that the family will keep the property.

What happens after my parent dies?

The loan generally becomes due after a maturity event described in the loan documents. The estate or heirs should contact the servicer promptly to understand the balance, requirements, available options, and applicable deadlines.

Can the heirs simply take over the reverse mortgage?

Generally, the reverse mortgage is not assumed and continued in the same manner by the heirs. They may need to sell the property, repay or refinance the amount required to retain it, or pursue another available option under the loan terms.

Does a reverse mortgage eliminate property taxes and insurance?

No. The borrower remains responsible for required property charges, including applicable taxes and insurance.

Who should explain the inheritance consequences?

The mortgage professional can explain how the loan balance and repayment structure work. An estate-planning attorney, tax professional, and financial advisor may be needed to evaluate the wider effect on the family’s estate and planning goals.

Bring the Family’s Questions

You do not have to agree on everything before starting a conversation.

Bring your parent, the questions, and the concerns.

Russ can help explain how the loan works, what responsibilities remain, what may happen later, and which alternatives deserve consideration.

Disclosure

Important reverse mortgage information: A reverse mortgage is a loan secured by the home. Interest and other permitted charges generally accrue and are added to the loan balance over time, reducing the remaining home equity.

Scheduled monthly principal-and-interest payments generally are not required while the reverse mortgage remains in good standing. Borrowers must continue to occupy the home as their primary residence, maintain the property, and pay required property charges, including property taxes, homeowners insurance, applicable flood insurance, and homeowners association charges. Failure to meet these obligations may cause the loan to become due and payable.

The loan generally becomes due and payable after a maturity event described in the loan documents, which may include the last borrower selling the home, permanently leaving the property as a primary residence, passing away, or failing to meet required loan obligations.

The rights and obligations of borrowers, spouses, non-borrowing residents, estates, and heirs depend on the specific product, title, loan documents, borrower qualifications, program requirements, and individual circumstances.

Eligibility, available proceeds, costs, rates, payment options, spouse protections, heir options, non-recourse protections, and program availability depend on the specific loan, property eligibility, financial assessment, underwriting, counseling where applicable, market conditions, state availability, and program requirements.

This information is provided for general educational purposes and is not financial, investment, tax, legal, insurance, benefits-planning, or estate-planning advice. It is not a loan approval, guarantee of eligibility, or commitment to lend.

Russell Tunick

Mortgage Loan Originator | Reverse Mortgage Specialist

NMLS #305398

Powered by Go Rascal Inc. | NMLS #2072896

Equal Housing Lender

Cell: (917) 538-7177

Email: [email protected]