Know what remains part of the homeowner’s role.

A reverse mortgage may change the way a homeowner handles mortgage principal and interest.

It does not make the home free to own.

That distinction matters.

Scheduled monthly principal-and-interest payments generally are not required while a reverse mortgage remains in good standing. But property taxes, required insurance, maintenance, association charges, and other homeownership expenses continue.

Interest and other permitted loan charges also generally accrue and are added to the loan balance over time.

The simplest explanation is this:

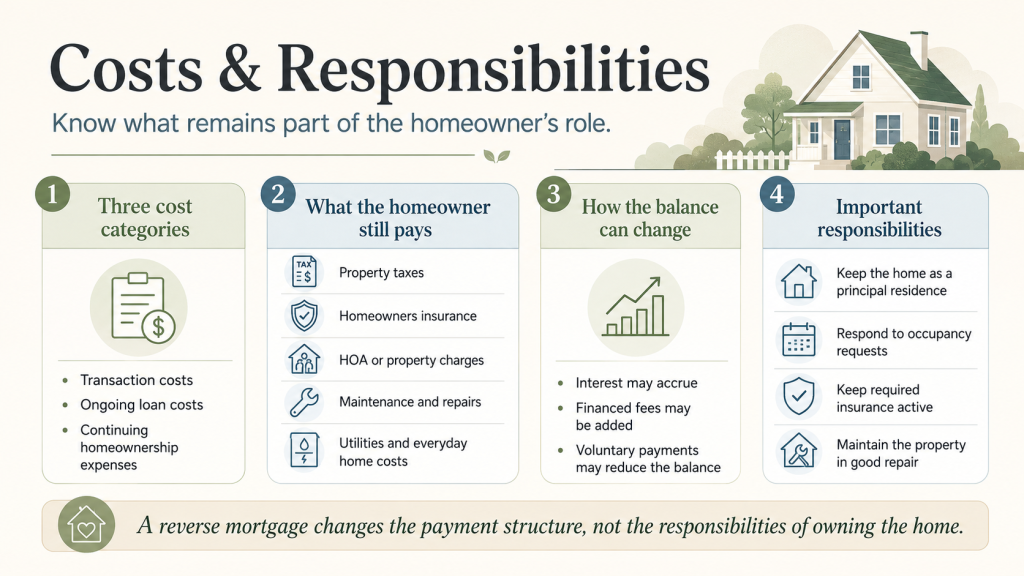

A reverse mortgage changes the payment structure. It does not remove the debt or the homeowner’s responsibilities.

Let’s walk through what that means in practical terms.

Three Types of Costs to Understand

It helps to separate the financial picture into three parts:

1. Transaction costs

These are costs associated with obtaining and closing the loan.

2. Ongoing loan costs

These may include interest, mortgage-insurance charges when applicable, and other permitted charges that affect the loan balance.

3. Continuing homeownership expenses

These are costs the homeowner remains responsible for because they continue to own and occupy the property.

Understanding all three gives the homeowner a clearer picture than focusing only on whether a scheduled monthly principal-and-interest payment is required.

Costs Connected With Obtaining the Loan

A reverse mortgage may include transaction costs such as:

- Origination charges

- Appraisal or other approved valuation costs

- Title search and title-insurance costs

- Settlement or closing services

- Recording and government charges

- Credit-report or verification costs when applicable

- Mortgage-insurance charges for a HECM

- Counseling-related costs when applicable

- Other permitted third-party or loan expenses

Not every charge applies in every transaction.

The exact costs depend on the loan product, property, lender, location, and individual circumstances.

A homeowner should receive and carefully review the applicable loan disclosures before making a decision.

Paying Costs in Cash Versus Financing Them

Some transaction costs may be paid with the homeowner’s funds.

Some may be financed into the reverse mortgage, subject to the program and transaction.

Financing a cost does not make it disappear.

When a permitted cost is added to the loan:

- It increases the starting loan balance

- Interest may accrue on the financed amount

- It may reduce the proceeds available for another purpose

- It may reduce the home equity remaining later

A homeowner should ask for a clear explanation of:

- Which costs must be paid before or at closing

- Which costs may be financed

- How financing the costs affects the starting balance

- How much of the available proceeds will be used for fees, liens, repairs, or set-asides

- What may remain available afterward

Interest Is Still Charged

A reverse mortgage is a loan.

Interest generally accrues on the outstanding balance.

Because scheduled monthly principal-and-interest payments generally are not required while the loan remains in good standing, interest is typically added to the balance rather than paid through a required monthly mortgage payment.

That means the balance may increase over time.

The amount of interest that accrues can be affected by:

- The interest-rate structure

- The amount borrowed

- When proceeds are received

- The length of time the loan remains outstanding

- Other charges added to the balance

- Voluntary payments, if any

A homeowner should understand whether the rate is fixed or adjustable and which part of the loan balance earns interest.

How the Loan Balance Generally Changes

With a traditional mortgage, scheduled principal-and-interest payments generally reduce the balance over time.

A reverse mortgage usually works differently.

The balance may increase as:

- Loan proceeds are advanced

- Interest accrues

- Financed closing costs are added

- Mortgage-insurance charges accrue when applicable

- Other permitted charges are added

If the borrower makes voluntary payments, those payments may reduce the balance according to the loan terms and servicer procedures.

Without voluntary payments, however, the balance generally grows.

That growing balance usually reduces the amount of home equity that may remain later.

Voluntary Payments May Still Be Possible

The absence of a required scheduled principal-and-interest payment does not necessarily prevent a homeowner from making voluntary payments.

A homeowner who is considering voluntary payments should ask:

- Are partial prepayments permitted?

- Is there a prepayment penalty?

- How will the payment be applied?

- Should special instructions accompany the payment?

- How could the payment affect the balance?

- Could it affect an available line of credit?

- Where should the payment be sent?

- How will the payment appear on the account statement?

The actual loan documents and servicer instructions control.

Property Taxes Remain the Homeowner’s Responsibility

A reverse mortgage does not eliminate property taxes.

The homeowner must ensure that required property taxes are paid on time.

Failure to pay them may place the loan in default and may cause it to become due and payable.

Before closing, the lender may review the homeowner’s ability and willingness to manage future property charges.

The homeowner should budget for:

- Regular property-tax bills

- Possible increases in assessed value

- Changes in available exemptions

- Special assessments

- Changes after the death or departure of a spouse

- Any local charges connected to the property

Questions about exemptions, assessments, or tax consequences should be directed to the appropriate local authority or qualified tax professional.

Homeowners Insurance Must Continue

Required homeowners or hazard insurance must generally remain active.

The coverage protects both the homeowner and the property securing the loan.

The homeowner should understand:

- The required coverage

- Who receives insurance notices

- When premiums are due

- Whether premiums are expected to increase

- What happens if the insurer cancels or declines to renew the policy

- Whether the policy satisfies the servicer’s requirements

- Whether proof of coverage must be provided

A lapse in required insurance can create a serious loan problem.

The homeowner should respond promptly to notices from the insurer or loan servicer.

Flood Insurance May Be Required

When the property is located in an area where flood insurance is required, the homeowner must generally keep the required coverage in place.

Flood-insurance costs may change over time.

A homeowner considering a reverse mortgage should not assume that the current insurance expense will remain the same indefinitely.

Insurance availability and affordability should be part of the housing review—especially when the homeowner expects to remain in the property for many years.

Association Charges and Other Property Assessments Continue

Depending on the property, the homeowner may remain responsible for:

- Homeowners association charges

- Condominium association charges

- Cooperative or community fees

- Ground rents

- Special assessments

- Municipal or other property-related charges

A reverse mortgage does not replace these obligations.

If an association is planning a major assessment or substantial increase, that information may affect whether the property remains affordable.

The homeowner should review recent association documents, budgets, notices, and meeting information when appropriate.

The Home Must Be Maintained

The property must generally be kept in good repair.

This does not mean the home must be perfect.

It means the homeowner must address conditions that could affect the property’s safety, habitability, value, or compliance with the loan requirements.

Maintenance may include:

- Roof and structural repairs

- Plumbing and electrical issues

- Heating or cooling systems

- Water intrusion

- Safety hazards

- Exterior deterioration

- Required pest or environmental work

- Local code issues

- Other repairs identified by the lender or servicer

The homeowner should budget for routine maintenance as well as larger, less predictable repairs.

A home that is affordable today may become difficult to maintain later.

That possibility belongs in the conversation before closing.

Repairs May Be Required Before or After Closing

The appraisal or property review may identify repairs that need to be completed.

Depending on the product and circumstances:

- Repairs may be required before closing

- Funds may need to be reserved for approved work

- The homeowner may need to complete work within a stated period

- Inspections or documentation may be required

- A transaction may not proceed if the property does not meet the applicable standards

After closing, the servicer may also require the homeowner to correct significant maintenance concerns under the loan terms.

The homeowner should understand who pays for the work, which deadlines apply, and how completion must be documented.

The Home Must Remain the Principal Residence

A reverse mortgage is generally tied to the homeowner’s primary residence.

That means the property must remain the borrower’s main home under the applicable loan rules.

A permanent move may cause the loan to become due and payable.

Extended absences may also require review, particularly when the homeowner:

- Enters a hospital or rehabilitation facility

- Moves temporarily to receive care

- Spends long periods with family

- Divides time between several homes

- Moves into assisted living or another residence

- Rents the property to someone else

A homeowner should contact the servicer when circumstances may affect occupancy rather than making assumptions.

Occupancy May Need to Be Confirmed

For a HECM, the borrower may be asked to certify periodically that the property remains their principal residence.

Ignoring an occupancy request can create avoidable problems.

The homeowner should:

- Open and review mail from the servicer

- Complete required occupancy certifications

- Keep contact information current

- Notify the servicer of relevant changes

- Retain copies of submitted documents

- Ask questions when a notice is unclear

Administrative responsibilities may sound small, but missing a notice can have serious consequences.

The Financial Assessment

Before approving a reverse mortgage, the lender may complete a financial assessment.

This review is designed in part to determine whether the homeowner appears able and willing to meet ongoing property obligations.

The assessment may consider information such as:

- Income

- Assets

- Existing debts

- Credit history

- Property-charge payment history

- Residual income

- Other program requirements

The financial assessment is not simply about whether the homeowner receives proceeds.

It also examines whether the home’s continuing expenses appear manageable.

A Set-Aside May Be Required

In some transactions, a portion of the available reverse mortgage funds may be set aside to help pay certain property charges, such as taxes and insurance.

This is sometimes called a Life Expectancy Set-Aside, or LESA, in the HECM context.

A set-aside may:

- Reduce the funds otherwise available to the homeowner

- Cover all or part of certain expected property charges

- Be administered according to the loan terms

- Last for a projected period rather than guaranteeing every future charge

The homeowner still needs to understand which expenses are covered, which are not, and what happens if the reserved funds are no longer sufficient.

A set-aside does not eliminate the homeowner’s obligation to ensure required charges are paid.

An Existing Mortgage Generally Must Be Addressed

When a homeowner already has a mortgage or certain other liens, those obligations generally must be satisfied as part of the reverse mortgage transaction.

The reverse mortgage proceeds may be used first to pay:

- The existing mortgage

- Certain required liens

- Closing costs

- Approved repairs

- Required set-asides

- Other permitted transaction expenses

Only after the required items are addressed would any remaining proceeds be available under the selected loan structure.

A homeowner should not assume that the difference between the home’s value and current mortgage balance will be available in cash.

Utilities and Everyday Living Expenses Continue

A reverse mortgage does not pay every cost associated with living in the home.

The homeowner continues to manage expenses such as:

- Electricity

- Water and sewer

- Heating fuel or natural gas

- Internet and telephone services

- Trash collection

- Landscaping

- Pest control

- Security services

- Household assistance

- Routine upkeep

These costs may increase over time.

A realistic aging-in-place budget should include more than the mortgage and property taxes.

Accessibility and Future Care Costs Are Separate

A homeowner may need future modifications such as:

- Grab bars

- Wider doorways

- Ramps

- Stair lifts

- Bathroom changes

- Improved lighting

- First-floor living arrangements

The homeowner may also need household help or personal care.

A reverse mortgage does not guarantee that enough funds will be available for every future housing or care expense.

The family should consider whether the home will remain physically and financially workable as needs change.

The Loan Servicer Has an Ongoing Role

After closing, the loan is managed by a servicer.

The servicer may:

- Send account statements

- Track the loan balance

- Request occupancy certification

- Monitor property taxes and insurance

- Process permitted advances

- Receive voluntary payments

- Issue notices about missing obligations

- Provide payoff information

- Communicate after a maturity event

The homeowner should keep the servicer’s contact information accessible and read all correspondence carefully.

Questions about the account should be directed to the servicer rather than left unanswered.

Keep Records Organized

A homeowner or trusted family member may want to maintain a file containing:

- The loan agreement

- Closing disclosures

- Counseling certificate

- Current insurance policies

- Property-tax receipts

- Association payment records

- Repair documentation

- Servicer statements

- Occupancy certifications

- Notices from the lender or servicer

- Contact information for key professionals

- Estate and title documents

Good records can make it easier to answer questions and respond to notices.

What Can Cause the Loan to Become Due?

A reverse mortgage generally becomes due and payable after a maturity event described in the loan documents.

Examples may include:

- The last borrower sells the home

- The last borrower permanently leaves the property as a primary residence

- The last borrower passes away

- Required property taxes are not paid

- Required insurance is not maintained

- The property is not maintained as required

- Other material loan obligations are not met

The specific loan documents control.

A homeowner should ask for a plain-English explanation of every event that may cause the loan to become due.

Missing an Obligation Can Have Serious Consequences

Failure to satisfy required obligations may place the loan in default.

That does not mean every mistake immediately results in foreclosure.

It does mean the homeowner should act quickly.

When a notice arrives:

- Read it carefully.

- Confirm the reason for the notice.

- Contact the servicer.

- Request written clarification when necessary.

- Keep copies of every communication.

- Seek approved housing counseling or qualified legal help when appropriate.

- Do not ignore deadlines.

Waiting can make a manageable issue more difficult.

What Happens When the Loan Becomes Due?

When the loan becomes due, it generally must be repaid.

Depending on the circumstances, this may occur through:

- Sale of the home

- Repayment from other resources

- Refinancing

- An option available to the estate or heirs under the loan terms

- Another permitted resolution

The exact options, amounts, notices, and deadlines depend on the product and circumstances.

The borrower, estate, spouse, or heirs should communicate promptly with the servicer after a maturity event.

Spouses and Other Residents Need Clear Information

A person living in the home does not automatically have the same rights as a borrower.

Important questions include:

- Who is a borrower?

- Who owns the property?

- Is a spouse a borrower or non-borrowing spouse?

- What protections may apply?

- Which conditions must continue to be met?

- What happens to another resident after the borrower moves or dies?

- Can the remaining person afford the property expenses?

These questions should be addressed before closing.

Title, trust, spouse, occupancy, and estate questions may also require qualified legal advice.

Responsibilities Do Not End When Family Members Become Involved

Adult children may offer help with:

- Reviewing mail

- Tracking tax and insurance due dates

- Coordinating maintenance

- Attending educational meetings

- Keeping records

- Communicating after a major life event

That support can be valuable.

But family involvement should be organized clearly.

The family should know:

- Who is responsible for each expense

- Who has legal authority to act

- Whether a power of attorney exists

- Where important documents are stored

- Who should contact the servicer

- What happens if the homeowner can no longer manage the property

Informal assumptions can create problems later.

Create a Realistic Annual Home Budget

A useful home budget may include:

Fixed or recurring expenses

- Property taxes

- Homeowners insurance

- Flood insurance when required

- Association charges

- Utilities

- Landscaping

- Routine services

Maintenance reserve

- Appliances

- Plumbing

- Electrical work

- Heating and cooling

- Roof repairs

- Exterior work

- Safety improvements

Future planning

- Accessibility modifications

- Household assistance

- Transportation

- Emergency repairs

- Insurance increases

- Special assessments

A homeowner should understand whether these costs remain manageable without relying solely on the absence of a scheduled principal-and-interest payment.

Questions to Ask Before Closing

A homeowner should feel comfortable asking:

- What costs will I pay before or at closing?

- Which costs will be financed?

- What will my starting loan balance be?

- How will interest be calculated?

- Which other charges may be added to the balance?

- Which property expenses remain my responsibility?

- Is a set-aside required?

- Which expenses will the set-aside cover?

- What repairs are required?

- What does principal residence mean under this loan?

- How will occupancy be confirmed?

- May I make voluntary payments?

- What could cause the loan to become due?

- What happens if I cannot pay taxes or insurance?

- What happens if I need to move?

- What should my spouse and children understand?

- Who will service the loan?

- Who should I call after closing?

A clear answer should come before the signature.

A Responsibility Checklist

Before deciding, confirm that the homeowner understands:

- The reverse mortgage is a loan

- The home secures the debt

- Interest and permitted charges generally accrue

- The loan balance generally increases

- Property taxes continue

- Required insurance continues

- Association and other property charges continue

- The home must remain the primary residence as required

- The property must be maintained

- Occupancy requests and servicer notices must be answered

- The loan eventually becomes due and payable

- Spouses, residents, heirs, and the estate may be affected

- Costs financed into the loan reduce equity and may reduce available proceeds

- Another option may be more appropriate

If any of those points remain unclear, the conversation is not finished.

The Bottom Line

A reverse mortgage may remove the requirement for scheduled monthly principal-and-interest payments while the loan remains in good standing.

It does not remove:

- Property taxes

- Insurance

- Maintenance

- Association charges

- Utilities

- Loan interest

- Other permitted charges

- Occupancy requirements

- Repayment

The homeowner retains title, but ownership comes with responsibilities.

The best time to understand those responsibilities is before the loan closes—not after a notice arrives.

Frequently Asked Questions

Are there no monthly payments with a reverse mortgage?

Scheduled monthly principal-and-interest payments generally are not required while the loan remains in good standing. Property taxes, insurance, association charges, maintenance, utilities, and other homeownership expenses continue.

Does interest still accrue?

Yes. Interest generally accrues on the outstanding loan balance and is added to the balance unless paid through voluntary payments or otherwise addressed under the loan terms.

Who pays the property taxes?

The homeowner remains responsible for ensuring required property taxes are paid, whether paid directly or through an approved set-aside arrangement.

Who pays the homeowners insurance?

The homeowner remains responsible for maintaining the required coverage. Depending on the transaction, certain charges may be paid through an approved set-aside, but the homeowner must ensure the obligation is satisfied.

What is a set-aside?

A set-aside reserves part of the available loan funds for certain future property charges. It may reduce the proceeds otherwise available and does not necessarily cover every property expense indefinitely.

Does the homeowner have to maintain the home?

Yes. The property generally must be kept in good repair according to the loan requirements.

Can the homeowner move away temporarily?

Temporary absences may be permitted under certain circumstances, but occupancy requirements vary. The homeowner should contact the servicer when an extended absence may affect principal-residence status.

Can voluntary loan payments be made?

They may generally be permitted, subject to the loan documents and servicer procedures. The homeowner should confirm how payments will be applied.

What happens if taxes or insurance are not paid?

The loan may enter default and could become due and payable. The homeowner should contact the servicer immediately after receiving a notice or realizing that a required charge cannot be paid.

Do the responsibilities transfer to the children?

The borrower remains responsible while the loan is active. Family members may help, but their authority and obligations depend on ownership, the loan documents, estate documents, and applicable law.

What is the best way to avoid problems after closing?

Understand the obligations before closing, maintain a realistic home budget, organize important records, respond to servicer notices, and ask for help promptly when circumstances change.

Closing Call to Action

Understand the Responsibilities Before Making the Decision

Bring the questions to Russ.

Russ can help explain the mortgage costs, continuing property expenses, occupancy requirements, and events that may cause the loan to become due.

Connect With Russ in the Way That Feels Most Comfortable

Use the link below to:

- Schedule a conversation on Russ’s calendar

- Call Russ

- Send Russ a general question

- Request the next step

Disclosure

Important reverse mortgage information: A reverse mortgage is a loan secured by the home. Transaction costs may include origination charges, appraisal or valuation costs, title and settlement charges, recording charges, mortgage-insurance charges when applicable, and other permitted expenses. Actual costs vary by product, property, location, and individual transaction.

Interest and other permitted charges generally accrue and are added to the loan balance over time, reducing the remaining home equity. Costs financed into the loan increase the balance and may reduce the proceeds otherwise available.

Scheduled monthly principal-and-interest payments generally are not required while the reverse mortgage remains in good standing. Borrowers must continue to occupy the home as their primary residence, maintain the property, and pay required property charges, including property taxes, homeowners insurance, applicable flood insurance, homeowners association charges, and other applicable property assessments.

Failure to meet the loan obligations may cause the loan to become due and payable. The loan generally also becomes due after a maturity event described in the loan documents, which may include the last borrower selling the home, permanently leaving the property as a primary residence, or passing away.

A financial assessment and a full or partial set-aside for certain property charges may be required. A set-aside may reduce otherwise available proceeds and may not cover every continuing property expense.

Eligibility, available proceeds, costs, rates, payment options, repairs, set-aside requirements, spouse protections, and program availability depend on the specific product, borrower qualifications, property eligibility, financial assessment, underwriting, counseling where applicable, market conditions, state availability, and program requirements.

This information is provided for general educational purposes and is not financial, investment, tax, legal, insurance, benefits-planning, or estate-planning advice. It is not a loan approval, guarantee of eligibility, or commitment to lend.

Russell Tunick

Mortgage Loan Originator | Reverse Mortgage Specialist

NMLS #305398

Powered by Go Rascal Inc. | NMLS #2072896

Equal Housing Lender

Cell: (917) 538-7177

Email: [email protected]

Website: https://russelltunick.com